🏦 How Lenders Actually Underwrite Loans (Not What Borrowers Think) 🔍

🏦 How Lenders Actually Underwrite Loans (Not What Borrowers Think) 🔍

📊 Mortgage Underwriting Explained: DTI, DSCR & What Really Gets Approved 💡

How Lenders Actually Underwrite Loans (Not What Borrowers Think)

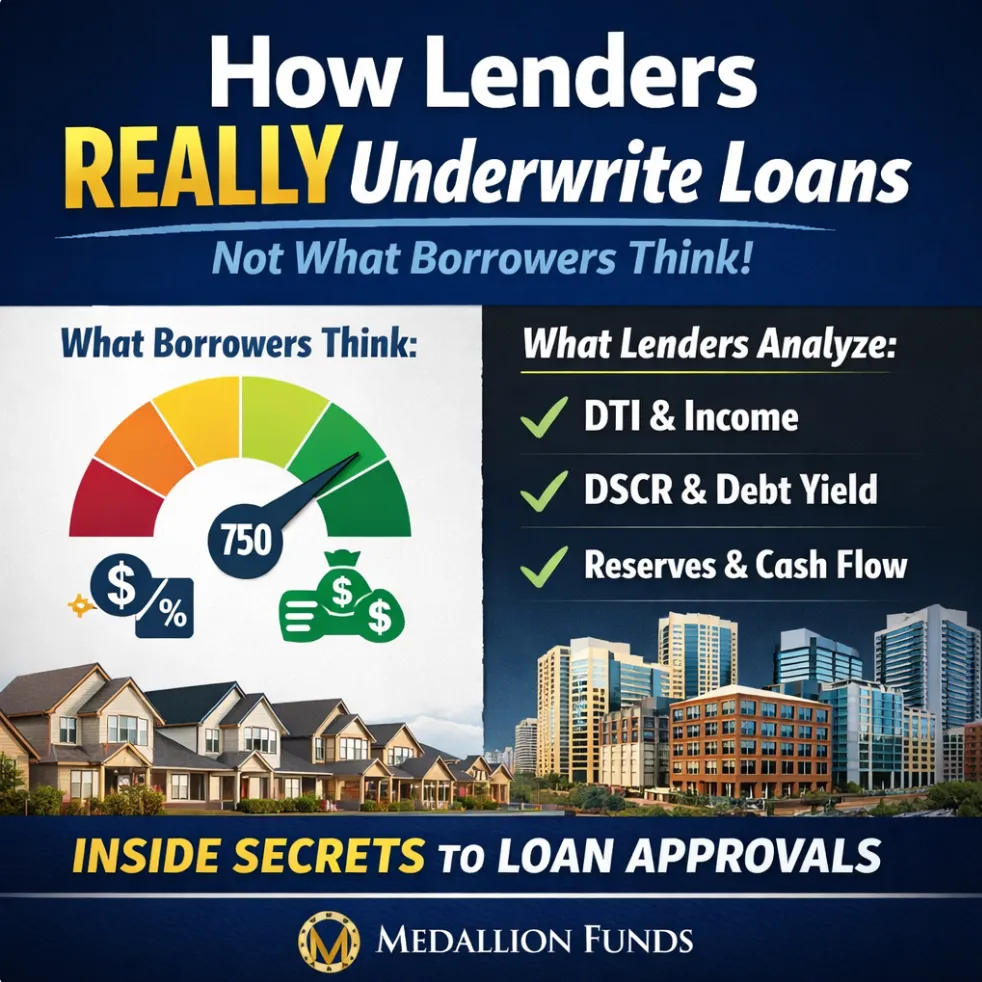

Most borrowers believe underwriting is about credit score and rate shopping.

It’s not.

Underwriting is about risk measurement, cash flow stability, and exit probability. Whether it’s a first-time homebuyer in Katy or a commercial investor refinancing in Houston, lenders use structured financial formulas—not emotion—to determine approval.

As a mortgage broker with access to hundreds of lenders through Medallion Funds, I see both sides: what borrowers think matters… and what lenders actually calculate.

Let’s break it down.

Residential Underwriting: What Really Matters

When underwriting a residential mortgage, lenders focus on three pillars:

1️⃣ Debt-to-Income Ratio (DTI)

DTI measures how much of your gross monthly income goes toward debt obligations.

Formula:

Total Monthly Debt ÷ Gross Monthly Income

Typical thresholds:

·Conventional loans: ~43–50% max DTI

·FHA loans: can stretch higher with compensating factors

·VA loans: flexible but still risk-based

What borrowers misunderstand:

·High income alone doesn’t fix high DTI.

·New car payments before closing can kill approvals.

·Installment vs revolving debt impacts differently.

Underwriters are analyzing repayment capacity, not just income level.

2️⃣ Income Types (And How They’re Calculated)

Not all income counts the same.

W-2 Borrowers:

·Averaged over 2 years if variable

·Bonus/commission requires documented history

Self-Employed Borrowers:

·Net income after deductions

·Add-backs allowed (depreciation, certain expenses)

·Typically 2-year average

Overtime, commissions, rental income, alimony—all have documentation standards.

The biggest misconception:

“I made this much last year, so I qualify.”

Underwriters qualify based on stable, continuable income, not gross deposits.

3️⃣ Reserves

Reserves are liquid assets remaining after closing.

Measured in:

Months of mortgage payments

Why reserves matter:

·Lower risk profile

·Offset higher DTI

·Strong compensating factor

A borrower with 6–12 months of reserves often receives stronger approval positioning than one with zero liquidity.

Commercial Underwriting: It’s About the Asset

Commercial lending flips the script.

Instead of focusing primarily on personal income, lenders focus on property performance.

Here are the key metrics:

1️⃣ DSCR (Debt Service Coverage Ratio)

Formula:

Net Operating Income (NOI) ÷ Annual Debt Service

Typical minimum:

1.20x – 1.30x

Example:

If a property produces $130,000 NOI and annual debt payments are $100,000:

DSCR = 1.30

That means 30% cushion above debt payments.

Lenders don’t ask:

“Can you afford it?”

They ask:

“Can the property afford itself?”

2️⃣ Debt Yield

Debt Yield = NOI ÷ Loan Amount

This measures lender risk independent of interest rate.

If NOI = $200,000 and loan = $2,000,000:

Debt Yield = 10%

Higher debt yield = lower lender risk.

Bridge lenders often focus heavily on debt yield thresholds.

3️⃣ Global Cash Flow

For business owners and real estate investors, lenders often analyze:

·Personal income

·Business income

·Real estate portfolio income

·Contingent liabilities

They combine everything to evaluate total financial strength.

This is called global underwriting.

If one property underperforms but the borrower’s overall financial picture is strong, approval can still happen—with the right lender.

Why Borrowers Get Confused

Borrowers assume:

·High credit score = guaranteed approval

·Big income = unlimited loan size

·Low rate = best deal

Lenders think:

·Is income stable and documented?

·Does the property cash flow?

·Is liquidity adequate?

·What is the exit strategy?

Underwriting is about probability of repayment.

Why Working With a Broker Changes the Game

A bank says:

“Yes” or “No.”

A broker asks:

“Which underwriting lane fits this borrower best?”

At Medallion Funds, we match:

·Self-employed borrowers → bank statement or alternative income lenders

·Investors → DSCR or portfolio lenders

·Business owners → global cash flow lenders

·Credit-challenged borrowers → structured bridge options

Underwriting isn’t one-size-fits-all.

It’s about understanding which lender sees your profile as low risk.

The Insider Truth

Approval isn’t about being perfect.

It’s about:

·Structuring correctly

·Positioning risk properly

·Choosing the right capital source

That’s the difference between:

❌ Getting denied

and

✅ Getting structured

If you understand how lenders actually underwrite loans, you stop guessing—and start preparing strategically.

That’s how sophisticated borrowers win.

— Bill Rapp

Medallion Funds

https://billrapponline.com/

https://www.billrapponline.com/

https://findamortgagebroker.com/Profile/WilliamRappJr28883

https://billrapp.commloan.com/

https://billrapponline.com/financingfuturescre-houston-katy

https://houstoncommercialmortgage.com/

https://author.billrapponline.com

https://doctorvideo.billrapponline.com/

https://veteransvideo.billrapponline.com/

https://mortgageviking.billrapponline.com/

https://fha203h.billrapponline.com/

https://renovationvideo.billrapponline.com

https://medallionfunds.com/bill-rapp/

https://www.amazon.com/dp/B0F32Z5BH2

https://veed.cello.so/FOmzTty6oi9

https://buymeacoffee.com/vikingente3

https://creplaybookseries.billrapponline.com

https://creplaybook.billrapponline.com/

© 2023-2024 Bill Rapp, Medallion Funds LLC, Director of Capital Advisory